When Free Cash Flow Loses Its Edge

What happens when the market starts rewarding cash burn? After more than a decade of profitability dominance in small caps, 2025 has delivered an unexpected twist.

- Small-cap stocks with positive free cash flow have historically outperformed cash-burning firms

- In 2025, this pattern reversed dramatically as speculative sentiment returned

- The current divergence is at historically extreme levels, suggesting mean reversion ahead

- Free cash flow discipline remains a key anchor for long-term equity performance

What happens when the market starts rewarding cash burn?

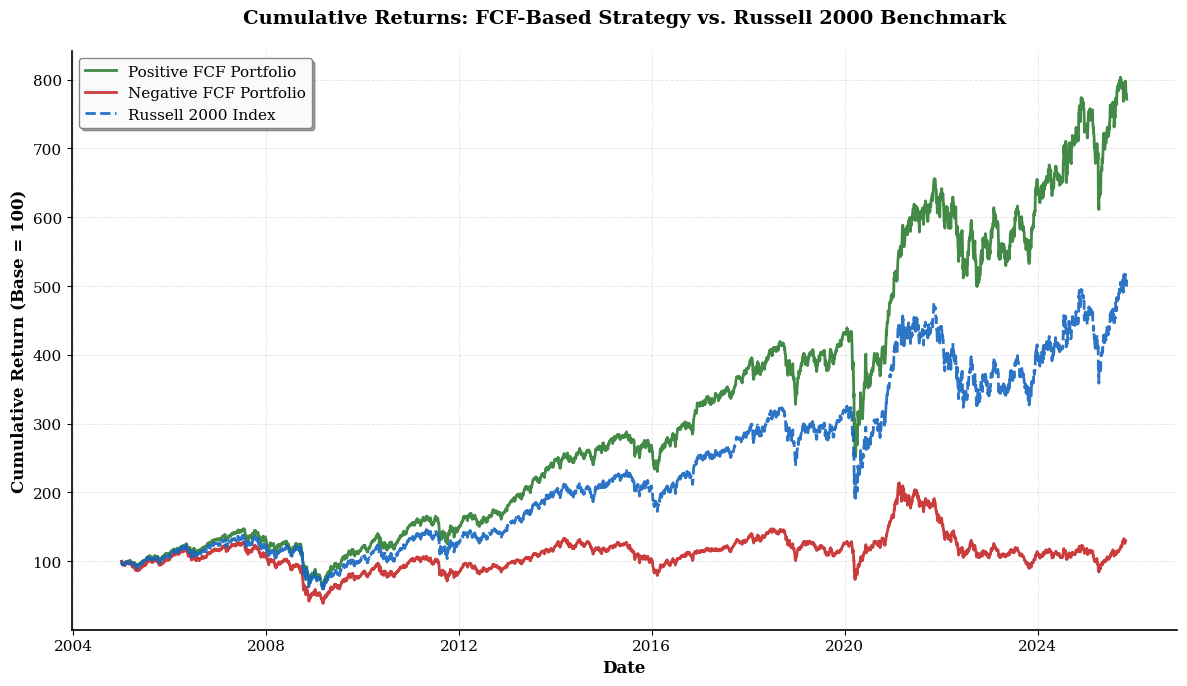

After more than a decade of dominance by profitable, cash-generating small caps, 2025 has delivered an unexpected twist. Within the Russell 2000 Index, the cohort of firms with positive trailing twelve-month free cash flow (FCF), long viewed as the bedrock of small-cap quality, has suddenly fallen behind their loss-making peers.

To illustrate this shift, we built two equal-weighted portfolios each month from the Russell 2000 constituents: one including only companies with positive FCF, and the other with negative FCF.

Historically, the difference could not be clearer. Investors who focused on profitable small caps, those funding their own growth rather than relying on external capital, have been rewarded with steadier compounding and lower volatility.

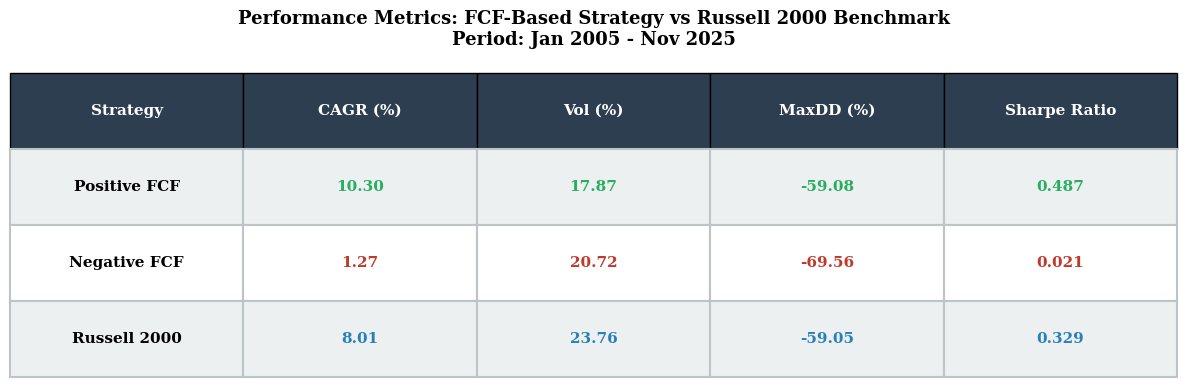

The summary statistics below confirm what many investors intuitively know: cash is king in the long run.

Across the full sample, positive FCF firms delivered superior annualized returns, higher Sharpe ratios, and smaller drawdowns. Negative FCF stocks, by contrast, earned their reputation as “junk” equities, high beta, high volatility, and poor long-term payoffs.

A 2025 Break in the Patterns

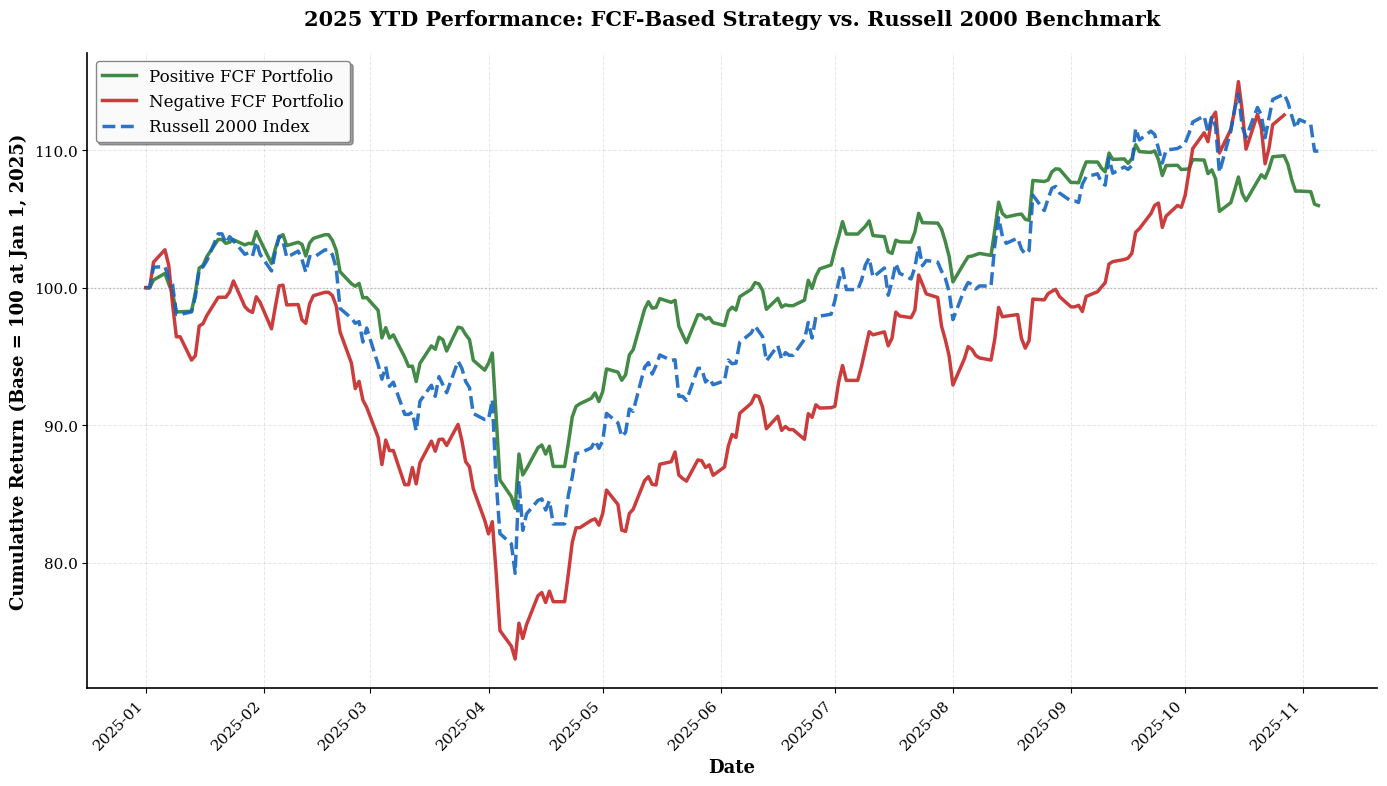

Then came April 2025.

A confluence of falling rates, easing financial conditions, and a resurgence in speculative sentiment sparked a sharp reversal. Suddenly, the market began rewarding companies that spent more than they earned.

From April onward, negative FCF stocks began to outperform their cash-flow-positive peers, first modestly, then decisively. By October, the cumulative returns of cash-burning firms had overtaken the disciplined, self-funding group for the first time in decades.

In other words, the market flipped: growth-at-any-cost was back in vogue.

An Extreme and Unsustainable Divergence

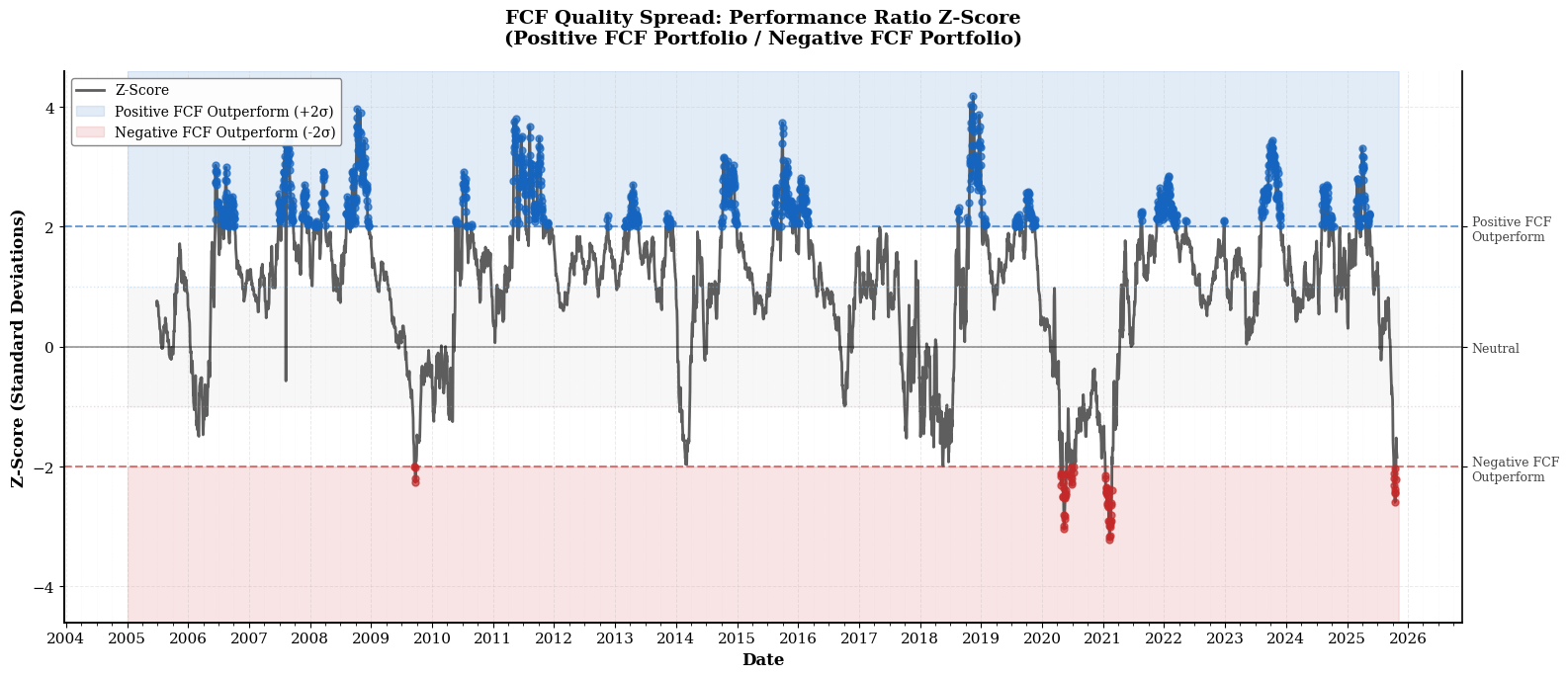

To assess how unusual this reversal has been, we calculated a 3-month rolling z-score of the return spread between positive and negative FCF portfolios.

The result? The current reading stands among the most extreme negative spreads in history, levels that, in past cycles, have consistently preceded mean reversion. Comparable episodes have only appeared during major liquidity-fueled rebounds: the 2009 post-crisis recovery, the 2020 COVID rebound, and the 2021 speculative “junk stock” rally.

Each of those periods was marked by a rush into unprofitable, high-beta names as investors chased cyclical or speculative momentum, yet all were short-lived. When speculative exuberance peaks, it rarely stays there. History suggests the pendulum soon swings back toward fundamental strength and cash-flow discipline.

The Cash Flow Gravity Principle

Free cash flow remains one of the most enduring anchors of long-term equity performance. While short-term rallies in unprofitable firms can occur during liquidity waves or bursts of optimism, they tend not to last.

Historically, episodes where negative FCF portfolios outperformed by this magnitude have been followed by sharp reversals in the following quarters as fundamentals reassert themselves. As investors, ignoring cash flow discipline may work for a season—but never for a cycle.

Enjoyed this note?

Get weekly curated research on systematic investing, asset pricing, and machine learning delivered to your inbox.